Most Indian founders register their GST when they have to, file for MSME when someone tells them to, and think about trademark “later.” By the time “later” arrives, a competitor has already filed your brand name. In 2024 alone, India saw over 5.4 lakh trademark applications — a 9.3% jump year-on-year — and a growing share of those are from D2C brands and small businesses who finally woke up to brand theft.

Here’s what nobody tells you: GST registration, MSME Udyam registration, and trademark filing aren’t three separate tasks. They’re one bundle — and doing them together saves you money, time, and a whole lot of future pain.

What You’ll Learn

- Why GST, MSME, and trademark work better as a bundle than as separate registrations

- The exact 50% trademark fee concession you get as an MSME — and how to claim it

- Step-by-step: what to do first, second, and third

- The real costs involved in 2025, with no surprises

- Answers to the most common founder questions about this compliance bundle

Why These Three Registrations Belong Together

Let’s break this down. Most founders treat compliance as a checklist — get GST when the accountant says so, register MSME someday, trademark when the budget allows. That approach costs you more in the long run.

Here’s the thing: your MSME Udyam Registration Certificate is the key that unlocks a 50% discount on trademark government fees. Without it, a private limited company pays ₹9,000 per trademark class. With a valid Udyam certificate, that drops to ₹4,500 per class.

File two classes for your brand name and logo — which most founders need — and you’ve saved ₹9,000 in government fees alone, just by getting MSME done first.

GST registration matters too, not just for tax compliance. When you file for MSME Udyam registration, the portal asks for your GSTIN (GST Identification Number). It isn’t always mandatory for businesses below the threshold, but having it makes the Udyam process smoother and positions your business as a credible, tax-compliant entity — something that matters when you’re applying for loans, government tenders, or payment gateway accounts with platforms like Razorpay.

The three registrations also reinforce each other for brand protection. Your GST certificate proves business existence. Your MSME certificate reduces your trademark filing cost. Your trademark protects the brand you’ve built. That’s the full compliance bundle — and it’s most powerful when done in order.

Step 1: GST Registration — What You Actually Need to Know

GST (Goods and Services Tax) is India’s unified indirect tax, introduced on 1 July 2017, replacing a maze of earlier taxes including VAT, service tax, and excise duty. If you’re selling goods or services in India beyond a certain threshold, you need to register on the GSTN (GST Network) portal.

As of 2025, the GST Council revised the mandatory registration threshold upward: ₹50 lakhs annual turnover for goods (previously ₹40 lakhs) and ₹25 lakhs for services (previously ₹20 lakhs). This change is expected to benefit over 1.2 million small businesses that previously had to comply unnecessarily.

That said, voluntary registration is often smart — it lets you claim input tax credit and signal credibility to B2B clients.

What most founders miss: even if you’re below the threshold, registering voluntarily gives your business a GSTIN, which makes the Udyam registration process cleaner, and signals to larger buyers and marketplaces that you’re a formal business.

You’ll need your PAN, Aadhaar, proof of business address, and bank account details to apply through the GST portal.

The Composition Scheme is also worth knowing: businesses with turnover up to ₹2 crore can now file returns annually instead of quarterly, reducing compliance load significantly. If you’re an early-stage founder in Bengaluru or Mumbai running a product business, this can save you hours every quarter. Lawizer’s compliance team handles GST registration and filing — from application to return filing — fully online.

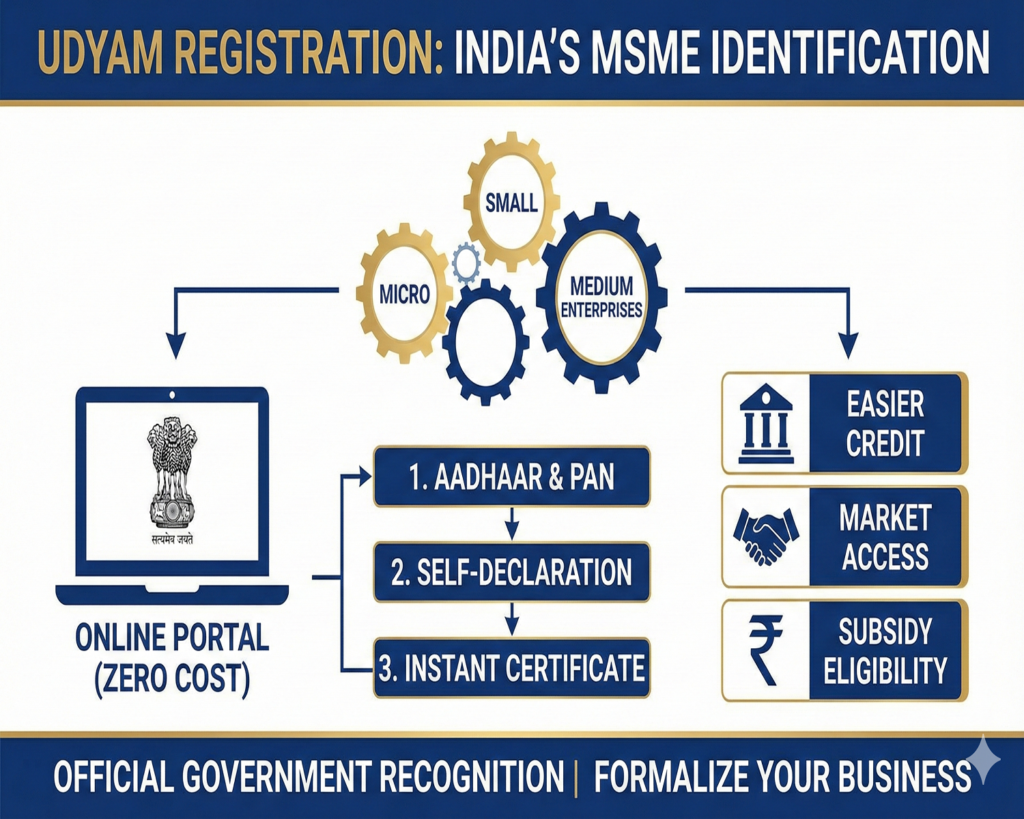

Step 2: MSME Udyam Registration — Your Compliance Multiplier

MSME stands for Micro, Small, and Medium Enterprise — a classification under the MSMED Act, 2006. As of 1 April 2025, the revised thresholds under Notification S.O. 1364(E) are as follows:

- Micro Enterprise: Investment up to ₹2.5 crore and annual turnover up to ₹10 crore

- Small Enterprise: Investment up to ₹25 crore and annual turnover up to ₹100 crore

- Medium Enterprise: Investment up to ₹125 crore and annual turnover up to ₹500 crore

Both the investment and turnover conditions must be met at the same time. Exceed either, and you lose MSME classification — along with its benefits. Registration happens through the Udyam Registration portal and is completely free of cost. You’ll need your Aadhaar, PAN, and GSTIN. The certificate is valid indefinitely and doesn’t need annual renewal.

A quick example: a D2C skincare startup in Kolkata with ₹15 lakh investment and ₹60 lakh annual turnover qualifies as a Micro Enterprise. Registering takes under 30 minutes online and immediately unlocks priority lending from banks, protection against delayed payments under the MSMED Act, and — crucially — the 50% trademark fee concession.

What most founders miss: Udyog Aadhaar (the older system, discontinued in 2020) does not qualify for the trademark fee concession. You need the Udyam Registration Certificate specifically. If you registered under the old system, migrate on the Udyam portal before you file your trademark. You can complete your MSME Udyam registration through Lawizer’s guided process — document collection, form filling, and certificate in hand, fully online.

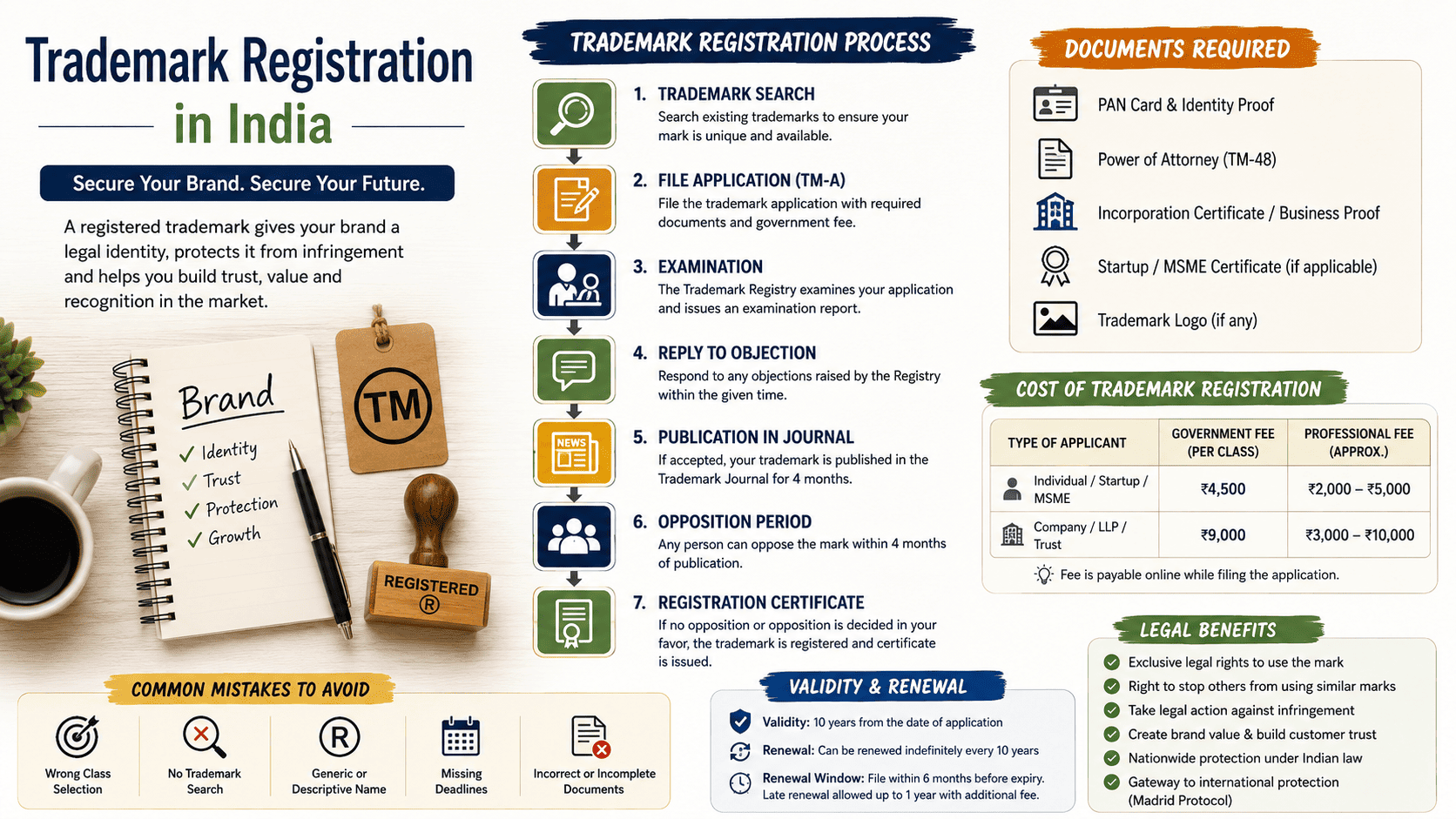

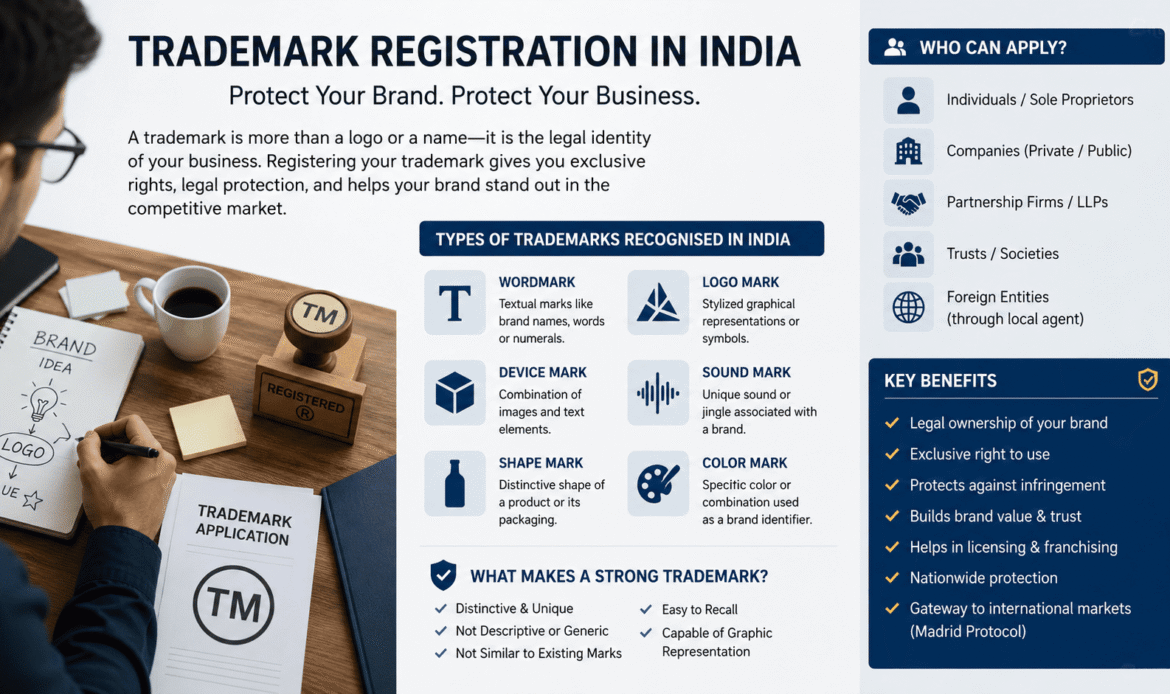

Step 3: Trademark Registration — Protect What’s Yours at Half the Cost

A trademark is the exclusive legal right to your brand name, logo, tagline, or any unique identifier — granted under the Trade Marks Act, 1999 and regulated by the CGPDTM (Controller General of Patents, Designs and Trade Marks) through the IP India portal. Here’s where your MSME certificate earns its keep.

Trademark Fee: MSME vs. Non-MSME (2025)

- With MSME/Udyam certificate: ₹4,500 per class (e-filing)

- Without MSME (Pvt Ltd, LLP, Partnership): ₹9,000 per class (e-filing)

That’s a straight 50% saving on government fees — applied at the time of filing, not as a reimbursement. You simply attach your Udyam certificate when submitting Form TM-A on the IP India portal. Let’s say you’re a food brand in Delhi filing under Class 29 (processed foods) and Class 30 (spices). With MSME: ₹4,500 × 2 = ₹9,000 in government fees. Without MSME: ₹9,000 × 2 = ₹18,000. Same protection, half the cost.

The TM symbol (™) can be used from the day you file. The ® symbol is only permitted after the registration certificate is issued — typically 18 to 24 months after filing under 2025 timelines, subject to examination and opposition. Note: professional fees charged by trademark agents are subject to 18% GST. Always confirm whether a service provider’s quoted price is GST-inclusive or GST-exclusive. For end-to-end filing, explore Lawizer’s trademark registration service — class selection, filing, and objection response included.

The Right Order: What to Do First, Second, Third

Sequence matters. Here’s the order that makes the most financial and legal sense:

- First — Get GST registration. Even if voluntary, your GSTIN is needed for cleaner Udyam filing and signals business formality to banks and buyers.

- Second — Get MSME Udyam registration. Free, takes under 30 minutes, and unlocks your 50% trademark fee concession. You need this certificate in hand before you file your trademark.

- Third — File your trademark. With your Udyam certificate attached, you file at ₹4,500 per class instead of ₹9,000. Legal protection for your brand name dates back to the day of filing.

The entire bundle — GST + MSME + Trademark — can be completed in under a week if your documents are in order. Documents you’ll need across the three: PAN card, Aadhaar card, bank account details, proof of business address, and a clear JPEG or PNG of your logo (for trademark filing).

Frequently Asked Questions

Q: Do I need GST registration before I can apply for MSME Udyam?

A: GST registration is not strictly mandatory for Udyam registration, especially if your turnover is below the GST threshold of ₹50 lakhs (goods) or ₹25 lakhs (services). However, having a GSTIN makes the Udyam application smoother and more complete. Voluntarily registering for GST before filing Udyam is strongly recommended, especially if you plan to file a trademark next.

Q: How much does the MSME trademark fee discount actually save me?

A: The discount cuts the government filing fee from ₹9,000 to ₹4,500 per trademark class for MSME-registered businesses. If you’re filing in two classes — which most brands need for their name and logo — that’s a direct saving of ₹9,000. The concession is applied at the time of filing Form TM-A by attaching your Udyam Registration Certificate.

Q: Can a private limited company get the MSME trademark fee discount?

A: Yes — if the company holds a valid Udyam Registration Certificate and its investment and turnover fall within the MSME classification thresholds. Entity type alone doesn’t determine eligibility; the Udyam certificate does. A private limited company that qualifies as a small enterprise under the MSMED Act 2006 is entitled to the ₹4,500 e-filing rate per class.

Q: What happens if I file a trademark without MSME registration?

A: You pay the full ₹9,000 government fee per class instead of ₹4,500. There’s no way to claim a retroactive refund on this difference after filing. Get your Udyam certificate first — it’s free, fast, and the savings on trademark fees alone justify the effort.

Q: How long does the entire GST + MSME + Trademark bundle take?

A: GST registration typically takes 7–10 working days after document submission. Udyam registration is almost instantaneous — the certificate is generated on the same day in most cases. Trademark filing can be done within a day of Udyam certificate receipt. The TM symbol is available from the day you file. Full trademark registration takes 18–24 months depending on examination and opposition, but your legal rights date back to the filing date.

Q: Is there any government subsidy for MSME trademark fees beyond the 50% discount?

A: Yes. The MSME IPR (Intellectual Property Rights) scheme provides reimbursement of 50% of the official filing fee actually paid, up to a specified ceiling. This is separate from the reduced fee concession and is not automatic — you need to submit a separate application with your fee receipt. Many founders miss this because they aren’t aware it exists. Check the MSME Ministry’s current scheme notifications for the latest ceiling amounts.

Lawizer’s experts handle everything — GST registration, MSME Udyam filing, and trademark registration — fully online, starting at just ₹999. No CA visit needed.