Introduction

The Indian crypto landscape has traveled a long road from the uncertainty of 2018 to the structured—yet stringent—regulatory framework of 2026.

As Virtual Digital Assets (VDAs) become a mainstay in the portfolios of Indian retail investors and institutional players alike, staying compliant is no longer just about avoiding penalties; it is about protecting your digital wealth.

With the Union Budget 2026 introducing refined definitions for Decentralized Finance (DeFi) and cross-border transactions, the tax authorities are watching more closely than ever.

This guide breaks down everything you need to know about navigating crypto taxes in India this year.

The Core Tax Architecture: The 30% Rule

Since the introduction of Section 115BBH in the Income Tax Act, the fundamental rule for crypto taxation in India has remained consistent.

The Flat Tax Rate

Income from the transfer of any Virtual Digital Asset is taxed at a flat rate of 30%, regardless of your income tax slab.

- No Deductions: Only the cost of acquisition is allowed. Expenses like electricity or platform fees cannot be claimed.

- No Loss Set-off: Losses from one crypto asset cannot be adjusted against gains from another.

The 1% TDS Mandate

A 1% Tax Deducted at Source (TDS) under Section 194S is applicable on transactions exceeding ₹50,000 annually for specified persons.

New for 2026: The Global Reporting Standard

India has integrated with the Crypto-Asset Reporting Framework (CARF).

The Income Tax Department now receives transaction data from international exchanges.

This means offshore holdings are no longer invisible to regulators, and global compliance is now mandatory.

Classifying Different Crypto Activities

Taxation varies depending on how you engage with crypto assets:

- Staking & Yield Farming: Taxed as “Income from Other Sources” at the time of receipt.

- Airdrops & Gifts: Taxable if value exceeds ₹50,000.

- Mining: Cost of acquisition is considered zero, making full sale value taxable.

Why Compliance is Getting Complex: The PMLA Factor

Crypto transactions now fall under the Prevention of Money Laundering Act (PMLA).

Investors must maintain detailed records, including wallet addresses and transaction logs, for at least six years.

How Lawizer Simplifies Crypto Compliance

Tracking crypto transactions across exchanges and DeFi platforms can be overwhelming.

Lawizer provides a streamlined solution for managing crypto tax compliance and audit readiness.

Why Choose Lawizer?

- Automated Audit Trails: Generates tax-ready reports based on latest compliance rules.

- PMLA Compliance Support: Ensures AML and KYC adherence.

- Legal Review: Helps ensure tokens and smart contracts align with regulatory guidelines.

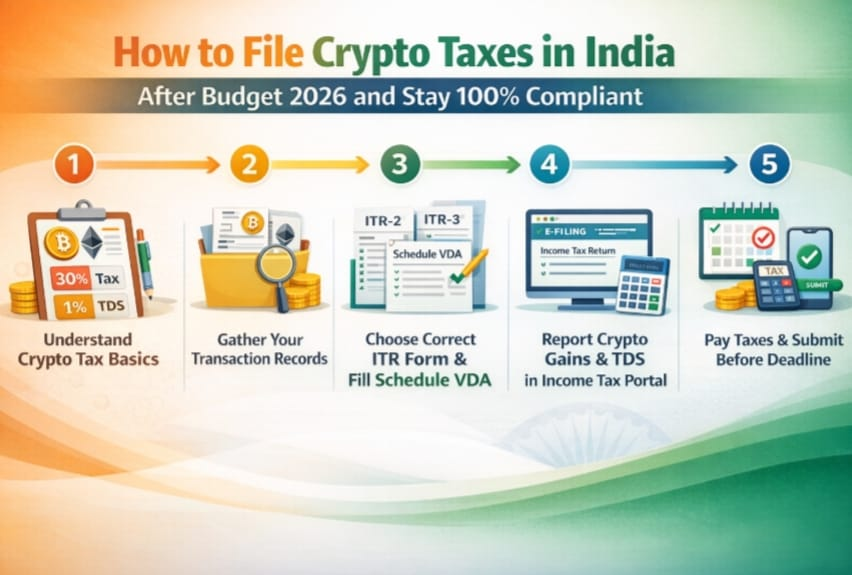

Filing Your Returns: ITR-2 and ITR-3

When filing your Income Tax Returns (AY 2026–27), ensure accurate reporting:

- Schedule VDA: Report acquisition and transfer details.

- Schedule FA: Mandatory for foreign-held crypto assets.

Failure to disclose foreign assets may attract penalties up to ₹10 lakh under applicable laws.

The Road Ahead: Regulation vs Innovation

India is moving toward a “Regulate to Protect” approach under global frameworks like the G20 coordination model.

The Reserve Bank of India (RBI) is also advancing its Digital Rupee initiative, which will further define the future of digital assets.

Conclusion: Don’t Trade in the Dark

In 2026, transparency is essential for crypto investors. Compliance is no longer optional—it is critical for protecting your assets.

Using platforms like Lawizer ensures that your crypto investments remain legally secure and audit-ready.

Frequently Asked Questions

Is the 30% tax on crypto profits still mandatory in 2026?

A: Yes. Under Section 115BBH, crypto income is taxed at 30% plus surcharge and cess.

Can I offset losses between different cryptocurrencies?

A: No. Losses cannot be set off against gains from other VDAs.

What is the purpose of 1% TDS?

A: It helps the government track transactions and can be claimed as tax credit.

Do I need to report crypto held on foreign exchanges?

A: Yes. It must be disclosed in Schedule FA to avoid heavy penalties.

How is staking income taxed?

A: It is taxed at receipt as income and again at sale under capital gains rules.

Are crypto-to-crypto swaps taxable?

A: Yes. They are treated as transfers and taxed accordingly.